How Paytm Neutralized RBI’s PPBL License Blow

With migration of services and severance of ties with PPBL done months ago, the RBI license revocation helps Paytm ward off a “blackout” for users.

pixabay

Opinions expressed by Entrepreneur contributors are their own.

You're reading Entrepreneur India, an international franchise of Entrepreneur Media.

The Reserve Bank of India (RBI) earlier this week announced the cancellation of the banking license issued to Paytm Payments Bank (PPBL), marking the closure of a tumultuous period of over two years for the company.

For the uninitiated, PPBL is a payments bank, which means it can accept deposits with limits and facilitate payments and remittances, but cannot lend like conventional banks. Set up in 2017, PPBL is a joint venture between Sharma (51%) and One97 Communications (49%).

One97 Communications, the parent company of Paytm, had seemingly preempted the repercussions [read worst-case scenario] in early 2024 when the central bank initiated the action.

Paytm discontinued inter-company agreements with PPBL, ensuring the latter remained a separate entity and Paytm’s operations ran uninterrupted. This was preceded by Vijay Shekhar Sharma stepping down from his position as part-time non-executive chairman and board member of PPBL.

In March 2024, when PPBL was under the spotlight for regulatory action and management shuffles, Paytm wrote off Rs 227.1 crore worth of investment in the associate entity. The company at the time had mentioned “ongoing uncertainty” with the payments bank in its filings.

Notwithstanding minor reliefs from the central bank in between, the regulatory action also prompted Paytm to acquire the Third-Party Application Provider (TPAP) license under the multi-bank model, enabling it to facilitate UPI services.

Interestingly, a year ago or so, Sharma had expressed hope that the payments bank would be back in business soon.

“As far as the bank is concerned, which is a separate entity, now we are pretty much at an arm’s length so it should get sorted out soon… We’ve learnt our lessons and we’ve dramatically changed our approach towards the business,” Sharma told Bloomberg News.

Evidently, it did not happen.

PPBL: A Timeline of Key Events

*Vijay Shekhar Sharma is among 11 members to receive in-principle approval from RBI for payments bank in 2015.

*PPBL commences operations as a payments bank with effect from May 23, 2017.

*RBI directs PPBL to stop onboarding new customers with effect from March 11, 2022.

*Early 2024 (January & February), RBI imposes additional restrictions such as ban on future deposits, credits etc.

*March 2024: PPBL is separated from the group company, One97 Communications.

*Paytm writes off its investment of INR 227 crore in PPBL

*April 2026: RBI revokes PPBL’s payments bank licence.

Why did the RBI revoke the license?

Even as many saw it coming, the RBI note on the cancellation gives a clearer picture on the entire saga. Interestingly, the central bank referred to the “general character of the management” and failure to comply with the conditions, among other things.

Earlier in 2024, the central bank had flagged issues such as “persistent non-compliance” and “supervisory concerns”. The RBI is even stricter in its latest note.

The bank noted:

(i) The affairs of the bank were conducted in a manner detrimental to the interest

of the bank and its depositors. Thus, the bank is not complying with Section 22

(3) (b) of the BR Act.

(ii) The general character of the management of the bank is prejudicial to the

interest of depositors as also the public interest. Thus, the bank is not complying

with provisions of Section 22 (3) (c) of the BR Act.

(iii) No useful purpose or public interest would be served by allowing the bank to

continue as envisaged in Section 22 (3) (e) of the BR Act.

(iv)The bank failed to comply with the conditions stipulated in the Payments Bank

license issued to it, thereby violating the provisions of Section 22 (3)(g) of the

BR Act.

The impact or the lack of it!

Paytm in its latest filings stressed that the move has no direct impact on the company as it had already impaired its investment in PPBL as of March 31, 2024.

It further said: “As informed earlier, Paytm (One 97 Communications Limited) and its services, which have been operating without interruption, will continue to operate uninterrupted. These include the Paytm app, Paytm UPI, Paytm Gold and all

other services offered by its subsidiaries and associated companies such as Paytm QR, Paytm Soundbox, Paytm card machines, and Paytm Payment Gateway, Paytm Money among others.

We would point out to all stakeholders that this matter is related to PPBL, a separate entity, and any reference to this matter should be made solely in the context of PPBL, and not attributed to the Company.”

Industry watchers have also responded to the RBI move.

“Operationally, the impact on Paytm may be limited because the company had already migrated key services like UPI processing and merchant settlements to partner banks after RBI’s 2024 restrictions. But strategically, this is a major setback because Paytm has now lost the ability to position itself as a fully integrated fintech ecosystem with its own banking layer,” Vikram raichura – Founder & CEO of helo.ai by Vivaconnect told Entrepreneur India.

“Earlier, Paytm’s strength came from controlling the full stack — wallet, payments bank, merchant settlements, FASTag and financial services within one ecosystem. Now, it increasingly functions as a distribution and interface platform dependent on third-party banks. That reduces differentiation, especially when banks themselves are becoming digitally stronger. For merchants, payments alone are no longer enough reason to stay loyal to a platform. Paytm’s future USP will likely depend on merchant engagement tools, AI-led customer communication, lending partnerships, and commerce enablement rather than banking ownership,” he added.

According to Bernstein, the move will have no immediate effect on Paytm owing to severance of ties quite early, reports ET BFSI. Similarly, Bank of America noted that Paytm “had decoupled itself from PPBL & revamped its business model & doesn’t have any exposure/ material biz arrangements to PPBL,” and that “the current business of Paytm isn’t impacted by the ban.”

Jefferies too said that the “cancellation of Paytm Payments Bank’s license has low impact for Paytm.” It also pointed out that key movements like UPI migration and wallet shutdown had already concluded, enabling key Paytm services to remain operational.

Even as Paytm may remain a TPAP for a relatively longer time, it still has a strong presence in the market – according to the National Payments Corporation of India’s November data, Paytm was the third largest UPI player, behind Google (GPay) and PhonePe.

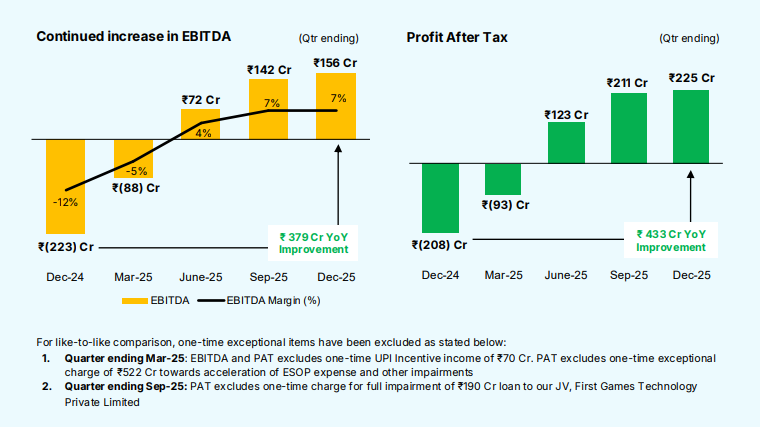

Paytm reported a revenue of INR 2,194 crore and a net profit of Rs 225 crore for the third quarter of the ongoing fiscal year (Q3 FY26). Operational revenue was up by 20% year-on-year from INR 1,828 crore in Q3 FY25. For the nine-months period, Paytm’s revenue was up by 24% to INR 6,173 crore from INR 4,989 crore, a year earlier, reports Entrackr.

Goldman Sachs reportedly expects Paytm to continue growing in the near future. The firm also maintained its “Buy” rating with expectation of another strong quarter. Paytm is scheduled to announce its Q4 2026 earnings on May 7.

That said, it is pretty much evident that Paytm has dodged the bullet by pre-emptive decision to decouple its services from the payments bank, write off the investment, and migration, among other things.

Though there are concerns that the company may face problems with securing future licenses from the central bank.

“For sure, it will not be easy to get approvals from the RBI and a few will be challenges for Paytm. To begin with, the greatest barrier is the deficit of trust in the regulator. RBI usually hardly ever steps in before long-standing problems with compliance in the areas of governance, KYC, and the treatment of data. The regulator is likely to demand a track record with full and open compliance before even thinking about issuing new licenses. Then, large improvements to internal controls, auditing and risk management are likely needed. Improvements can prove costly and mean an even longer wait before the company can reapply,” Siddharth Maurya, Managing Director, Vibhavangal Anukulkara Pvt Ltd told Entrepreneur India.

“Fintech laws are becoming tougher, the RBI is overly cautious with systemically important sectors which means that even if a platform like Paytm was successful, it would be treated with even more caution. Then, there is the reputational erosion. There is no doubt there would have to be a strict assessment in the future on the ability to govern which takes years to build trust. For the consumer, it means that while Paytm would be able to operate with systemically important sectors through other structures, full-stack licensing is a long way away,” he added.

It’s worth noting that the company’s Paytm Payments Services Limited (PPSL), bagged the RBI authorisation in December last year to act as a payment aggregator (PA) for both offline payments as well as cross-border transactions.

The Reserve Bank of India (RBI) earlier this week announced the cancellation of the banking license issued to Paytm Payments Bank (PPBL), marking the closure of a tumultuous period of over two years for the company.

For the uninitiated, PPBL is a payments bank, which means it can accept deposits with limits and facilitate payments and remittances, but cannot lend like conventional banks. Set up in 2017, PPBL is a joint venture between Sharma (51%) and One97 Communications (49%).

One97 Communications, the parent company of Paytm, had seemingly preempted the repercussions [read worst-case scenario] in early 2024 when the central bank initiated the action.